A Woman jogs past the U.S. Capitol in Washington, October 24, 2019.

Siphiwe Sibeko | Reuters

Washington can feel pretty gridlocked these days, with the impeachment proceedings against President Trump dividing politicians by party lines. Still, both Republicans and Democrats have rallied around a number of bills that could deliver real changes to your personal finances.

One measure would help Americans struggling with health-care expenses. Currently, your out-of-pocket health costs must be more than 10% of your income for you to claim the medical expenses tax deduction. The Medical Expense Savings Act would lower that threshold to 7.5%. Republican Sen. Susan Collins of Maine sponsored the bill, and two Democrats have co-sponsored it.

Only people who itemize their deductions qualify, and that number has dwindled with the doubling of the standard deduction.

Still, resetting the threshold to 7.5% would benefit more than 4.4 million people, according to The Institute on Taxation and Economic Policy. And it would save those over age 65 around $500 a year, according to AARP.

More from Personal Finance:

One retailer trick you don’t want to fall for this holiday season

What to know if you need some relief from medical debt

Why your vaping habit could raise your life insurance costs

Another piece of legislation with backing from both sides of the aisle — the Veterans and Consumers Fair Credit Act — would cap interest rates on consumer loans at 36%, a protection currently only available to active-duty service members. That rate might sound high, but some payday loans today come with interest rates of nearly 400%.

“It’s time for Congress to follow the Pentagon’s lead and extend the same rules that protect soldiers, sailors, airmen and marines from predatory loans to every Americans,” said Christopher Peterson, the director of financial services at the Consumer Federation of America.

A bill called the Pregnant Workers Fairness Act would require organizations with more than 15 employees to make reasonable accommodations to workers impacted by pregnancy or child birth, so long as those conditions don’t cause undue hardship for the business.

Helium Health’s medical records dashboard

Helium health

Last month, the U.S. House Committee on Education and Labor Civil Rights and Human Services Subcommittee heard testimony from Kimberlie Michelle Durham, who said she lost her job as an emergency medical technician after she requested an accommodation when she was pregnant.

“It’s wrong that something as normal and natural as becoming a parent cost me a career that I loved and was good at, and cost me my financial well-being,” Michelle Durham said.

A number of Republicans and Democrats are pushing for the bill.

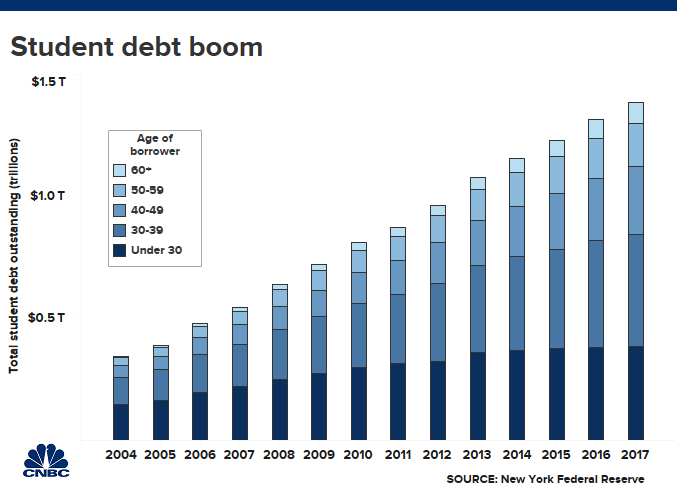

Legislation could also bring relief to student loan borrowers.

Republicans and Democrats have shown interest in reducing the number of student loan repayment plans to just two. There are currently 14 ways to repay your student loans, a complicated system critics say leads to needless defaults.

One plan would simply spread a borrower’s monthly payments across a decade. The other would cap monthly payments at a percentage of a borrower’s income, and their repayment timeline could be 20 or more years. There is also bipartisan support for eliminating origination fees on student loans.

At least one Republican, in addition to a host of Democratic lawmakers and presidential candidates, wants to allow student debt to be discharged in normal bankruptcy proceedings. Currently, borrowers have to exhibit a “certainty of hopelessness” to walk away from their student debt in court.

There’s no sound reason that struggling student loan borrowers shouldn’t be able to get a fresh start, said Mark Kantrowitz, a higher education expert.

“Credit cards can be discharged, but not student loans?” he said.

Changes could also be in store for your retirement savings. The Secure Act, which passed the House with overwhelming bipartisan support in May, would make more workers — including those who are part-time — eligible for retirement savings accounts. People would also be given more time before the IRS requires them to start spending down their nesat eggs.

The impeachment process currently underway in the House may have slowed that legislation, but experts say it’s not dead in the water.