That number was the third highest on record, despite the fact that the tax changes that took effect in 2018 reduced some of the opportunities to take advantage of tax breaks for charitable giving. Clearly, most donations are motivated by a lot more than tax savings. But there’s no reason not to maximize your tax benefits from being charitable and to do that, under the new law, takes some planning. Here are five key strategies. The best option will depend on your age, the amount and type of assets you plan to gift, and the level of control that you want to exert over the gift. As always, it’s smart to consult your own tax advisor.

The Tax Cuts and Jobs Act passed in December 2017 doubled the standard deduction (you can see the 2019 tax rates and other tax changes here), meaning many taxpayers have a reduced incentive to itemize. The most recent Internal Revenue Service data shows only about 10% of taxpayers claimed itemized deductions on their 2018 tax returns, compared to more than 30% who did so in the previous year, a difference of about 28 million taxpayers.

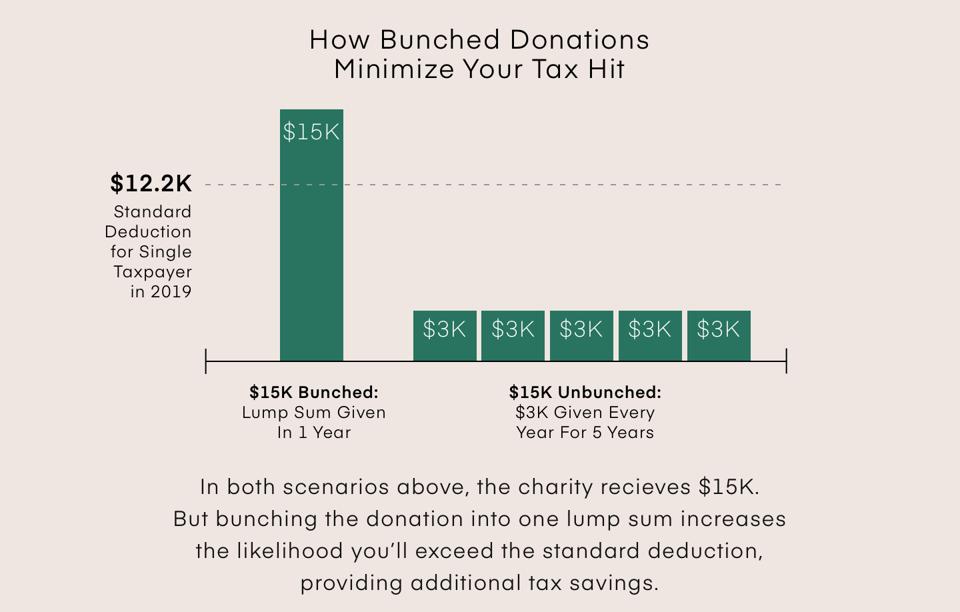

Since you must itemize to claim a charitable deduction, that means that fewer taxpayers will benefit by giving to charity in any one year. The solution? Consider bundling charitable gifts. With bundling, or bunching, you simply alter the timing of your charitable giving game plan to pack the biggest tax punch.

So, for example, instead of donating $3,000 annually for each of five years, consider giving $15,000 all at once. It’s the same total gift as before, but if you coordinate it with your other eligible itemized tax deductions such as real estate taxes and medical expenses, you can benefit by itemizing in the year you make your big donations, then claiming the standard deduction in other years.

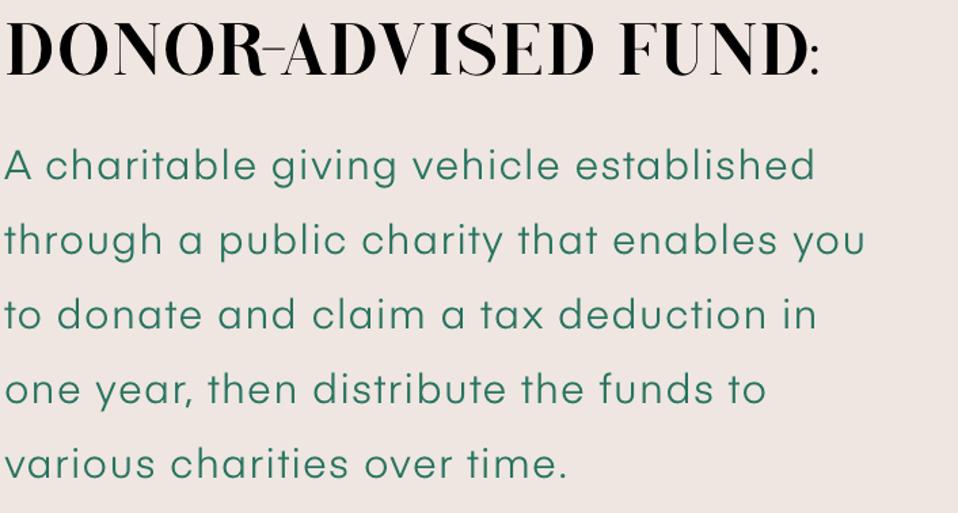

While donor-advised funds (DAFs) have been around for decades, interest in them has spiked because of the combination of tax benefits and degree of retained control they provide. Perhaps you want to participate in the annual fund drive at your church or favorite charity and the idea of bundling your contributions into one year out of five just to claim a tax deduction doesn’t appeal to you? The DAF provides a solution.

You can make a big contribution of cash, stock or other assets to a DAF in one year and receive a federal income tax deduction for your donation in that year.

Then, you can dribble out contributions to your favorite operating charities over time. Meanwhile, the assets within the DAF can be invested and grow income tax-free inside the fund—meaning you can use a DAF to establish a charitable legacy for your family, allowing your children, as they mature, to recommend which charities to support.

Since a sponsoring organization—which can be a charitable affiliate of a financial company, a local community foundation or a charity itself—must manage a DAF, you’re not directly responsible for management costs, keeping expenses minimal.

Just be careful: There’s no double-dipping. Since you get a federal income tax deduction for your initial contribution, subsequent distributions to charities from the DAF aren’t tax-deductible. Plus, you can’t use DAF money to, for example, pay for a charity dinner where you get something of value back. But you can increase your initial tax benefit by donating appreciated assets to a DAF, as described in Strategy #3.

Donating appreciated assets—like highly appreciated stocks—to charity is a tax-favored way to support your favorite charity. You get the benefit of a charitable deduction for the fair market value of the assets at the time of your contribution without paying capital gains tax on the appreciation.

Here’s how it works. Let’s assume you want to donate $1,000 of stock to charity, and you paid $100 for the stock. If you sell the stock before you donate it, you have $1,000, and you owe tax on the $900 capital gains (selling price of $1,000 less $100 cost basis). If you assume a 15% capital gains tax rate—since that’s what most taxpayers will pay—that’s $135 in tax. If you donate the after-tax gains to charity, the charity only gets $865, and you get a charitable deduction of $865. If, however, you give $1,000 of appreciated stock directly to the charity, you pay no capital gains tax and get the benefit of a charitable deduction worth $1,000. The charity would then sell the stock for $1,000 and pay no capital gains tax (remember, the charity is tax exempt) so that they keep the entire $1,000. It’s a win-win.

A couple of quick cautions: Capital gains tax rates can vary based on your income and the type of asset, so keep that in mind when running the numbers. Also, if the assets have decreased in value, it may make sense to sell first—and then make the donation; that way, you have a capital loss for tax purposes, and you still have the advantage of the donation deduction.

You can combine this strategy with a charitable trust for even more flexibility and control. When you contribute highly appreciated assets to an irrevocable trust, you’ll receive a charitable deduction for income tax purposes. The amount of the deduction is equal to the value of the charity’s right to receive either the remainder of the money after a particular term (a number of years or your lifetime) or the right to receive the income from the trust for a set number of years. You can get more details on trust options from a charity’s planned giving office or your own tax or estate lawyer.

Typically, if you want to make a charitable donation from your IRA, you’d have to withdraw those funds, pay the associated tax and then make the donation.

However, beginning in 2015, the tax laws changed to allow taxpayers age 70½ or older to transfer up to $100,000 annually from their IRA accounts directly to charity income tax-free. Even better: The transfer counts toward your required minimum distribution for the year.

To qualify as an eligible transfer, the funds must be directed by the IRA trustee to the charity; the transaction is sometimes referred to as a charitable rollover. If you pull the funds out yourself and write a personal check, it doesn’t qualify as a charitable rollover and is a taxable event. One additional note: You may not use a charitable rollover to make donations to DAFs, supporting organizations or private foundations.

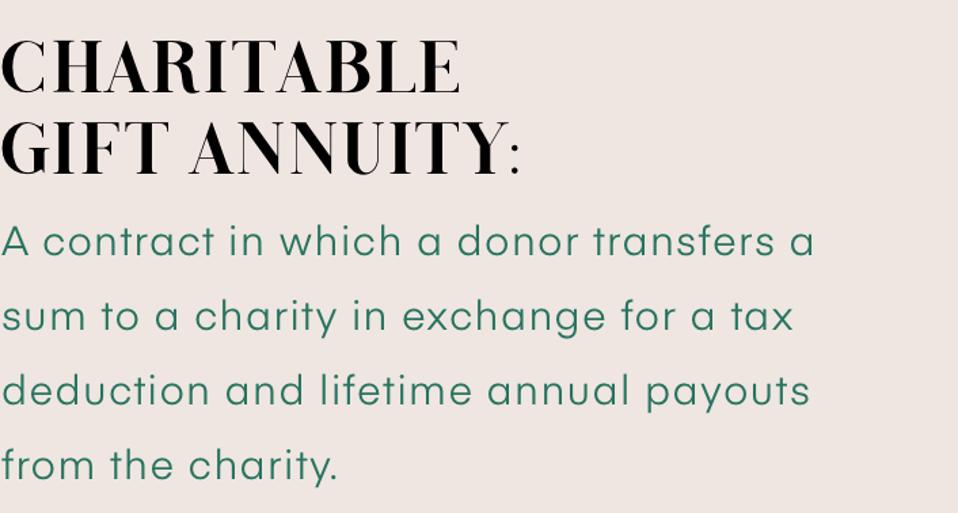

If you want to make a donation and receive a fixed source of income in return, consider a charitable gift annuity. An annuity is a contract that guarantees payments for a specific number of years. Here’s the charitable twist: you can enter into an agreement to make a lump-sum gift to a favorite charity in exchange for the right to receive fixed payments. The size of the payment is determined by a number of factors, including your age. The amount you’re entitled to receive doesn’t change, even if the investment dips on the charitable side. After the term of years—or if you die before the term expires—the charity gets to keep the cash.

You’re entitled to a federal income tax deduction for the value of your gift. The amount of the deduction isn’t your initial contribution but is an amount based on the right of the charity to receive the remainder at the end of the term. You may have to pay income tax on the payments you receive to the extent they represent interest (part may represent a return of principal).

One more thing: you’re not limited to a cash gift. Since the transfer is to charity, you can donate appreciated assets and escape capital gains tax (see above).