Stock market virus fear or bull and bear economic crisis and sick financial health as a business … [+]

Getty

Recessions are a normal part of the business cycle, albeit some are more severe than others. The current recession is expected to be the most severe since the Great Depression, which is not good for stocks. Are there lessons we can learn from past recessions? Yes. Does history ever repeat itself? Many times, it does.

In this article, by examining the past 14 recessions, we will answer the following questions:

· How long did each recession last?

· How severe was each recession?

· At what point during each recession did stocks hit bottom?

· How much did stocks lose from the start of each recession until they bottomed?

I’ve found some interesting trends from past recessionary periods that may be useful today. Keep reading as we uncover valuable information from the past 14 U.S. recessions.

How Long Did The Past 14 Recessions Last?

Recessions vary in terms of duration. The average length of the past 14 recessions was 403 days or about 1.1 years. When you exclude the Great Depression, this is reduced to 334 days. The longest was 1,307 days or about 3.5 years (Great Depression) and the shortest was the 1980 recession, which lasted 6 months. The following chart shows how long each of the past 14 U.S. recessions lasted. Again, excluding the Great Depression, the length of a recession ranged between 181 (1980) and 547 days (2007-09).

# Days of Past 14 Recessions

MJP

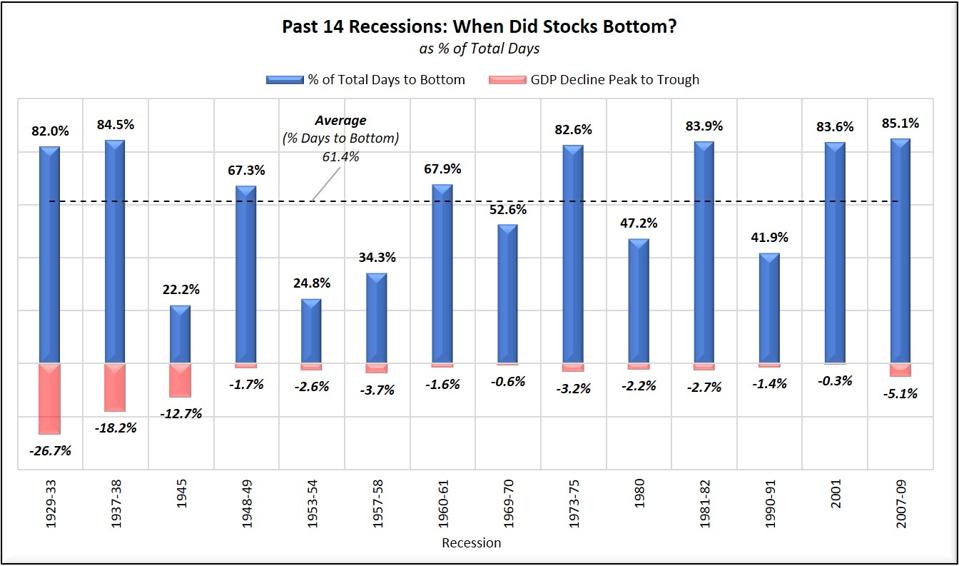

How Long Did It Take Stocks To Hit Bottom During a Recession?

Stocks have a strong tendency to lose value during a recession. This is primarily due to reduced corporate profits triggered by less consumer demand. Moreover, stocks tend to bottom during the latter half of a recession, as displayed in the following chart. The chart also shows the % of total days into the recession when stocks bottomed, the average length of time if took for all 14 periods, and the % drop in GDP from peak to trough. The GDP data illustrates the severity of each recession. As an example, if there were 100 days in a recession and stocks bottomed on day 80, then it can be stated that stocks bottomed when the recession was 80% complete. Here are the results.

During the 2007-09 recession, stocks hit bottom on March 9, 2009 when the recession was 85.1% complete. The shortest time was just after WWII when stocks bottomed 22.2% of the way through the downturn. On average, stocks hit bottom when the recession was 61.4% complete. In 8 of the 14 periods examined, stocks hit bottom in the last half of the recession. In six of those periods, stocks bottomed when the recession was over 80% complete. Thus, it can be said that stocks have a strong tendency to hit bottom closer to the end of a recession.

Past 14 Recessions-When Did Stocks Bottom

MJP

How Much Did Stocks Lose?

Another key question is: How much did investors lose from the start of a recession to the point when stocks bottomed? The next chart has the answer. It shows the maximum loss from the start of each recession to when stocks hit bottom. It also illustrates the decline in GDP from peak to trough, plus the average % decline in stocks for all periods. For example, during the most recent recession (2007-09), stocks fell 50.8% from the beginning of the recession (Dec 1, 2007) to March 9, 2009.

On average, stocks lost -25.5% during these recessions. When you exclude the Great Depression, this improves to -20.7%. Again, you can compare the losses with the severity of each period.

Past 14 Recessions-How Much Did Stocks Lose

MJP

Year 2020: Have Stocks Already Bottomed?

The DJIA peaked February 12, 2020, closing at a record high of 29,551. It then fell 37% by March 23. Since then, stocks have risen over 32% (as of April 29). After today’s trading (Apr 30), the DJIA is a little over 20% below its record high. Is the worst over? Have stocks already bottomed? Is there more pain to come? If we rely on the past 14 recessions for clues and consider the expected drop in GDP for the second quarter of 2020 (-40%), we might conclude that the worst is yet to come. Let’s explore this further.

The shortest recession of the previous 14 lasted only 6 months (1980). If this recession, which we assume began April 1, lasts six months, and if stocks bottom as early as they did during the 1945 recession, the bottom would come in around May 10. Is it possible that stocks have already hit bottom even though this recession is expected to be the worst since the Great Depression? That’s hard to imagine. There is, however, a significant tailwind this time.

The Fed: A Game Changer?

When it wants to increase or decrease the money supply, the Fed buys or sells only high-quality securities (U.S. Treasuries). In the 2007-09 recession, to the surprise of most, the Fed added mortgage-backed securities to the mix (after all, it was a mortgage crisis). This time, the Fed is pulling out all the stops, buying municipal bonds and even junk bonds. Is this important? Absolutely. If the Fed did not buy these bonds, there would be much less demand and the price of these bonds would drop. For example, if the price of junk bonds fell due to weak demand, the less credit-worthy companies would find it difficult to raise capital and defaults would spike. A spike in defaults would create a ripple effect, causing other securities to collapse, which would have a negative effect on the economy. Therefore, the Fed has implied that it will buy whatever is needed to support demand and stabilize the financial markets.

This type of action is not without precedent. During the ‘Panic of 1907’, and before the Federal Reserve existed, J.P. Morgan injected a large amount of his own capital into the system to help stabilize markets. You see, when selling pressure is greater than buying pressure (in aggregate), prices fall. The Fed is currently buying these securities to boost demand for the same reason. The million-dollar question is: Will the Fed be able to inject enough capital into the economy to minimize the pain? More to the point, this unprecedented infusion of monetary stimulus is removing money that would otherwise be available for future investment, spending, and savings, in order to provide relief today. It is, after all, an election year.

There is a tug-of-war between the administration’s monetary stimulus and the fear and economic turmoil from COVID-19. Who will win? The Fed will surely need to inject more money into the system. As it does, the federal debt will continue to swell, creating an even larger problem in the future (read more on this in my latest article: The Approaching COVID-19 Debt Crisis: How Excessive Debt Reduces Economic Growth). In short, the government is doing everything it can to minimize the severity of this crisis, but they do so at the peril of our future. Will it be enough? How much will it cost?

Stay tuned.