There’s an expense lurking down the road for many retirees that is largely unpredictable but likely: long-term care.

With premiums soaring on insurance policies designed to cover that cost, financial advisors are turning to a variety of other strategies to help clients prepare for a day when they might need help with daily living activities such as eating and bathing.

“The fact is we’re a country that excels at prolonging and extending life,” said Matthew Brennan, a certified financial planner and partner at Acorn Financial Services in Reston, Virginia. “The result is that the costs of care later in life, and the duration of the care, are lasting longer and longer.”

Terry Vine | Getty Images

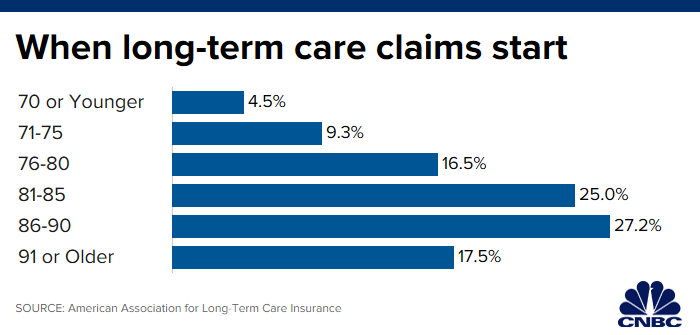

Someone turning 65 today faces a nearly 70% chance of needing LTC services during their remaining years, according to the U.S. Health and Human Services Department. On average, women need care longer (3.7 years) than men (2.2 years).

Related monthly costs can be eye-popping: a median $4,000 for care at an assisted-living facility ($48,000 yearly), $7,400 for a semi-private room in a nursing home ($89,000 a year), $4,200 for a home health aide ($50,400 annually) and $4,000 for homemaker services ($48,000 a year).

“Without planning, long-term-care costs can be a big financial hit,” said CFP Kelly Wright, director of financial planning for Columbia, Maryland-based Pinnacle Advisory Group, which ranked No. 80 on the CNBC FA 100 list of top advisor firms for 2019.

And, Medicare — relied on by most retirees — generally doesn’t cover LTC. (Skilled nursing care and rehabilitative services do get limited coverage related to certain hospital stays.)

For standard health care alone in retirement, the average 65-year-old couple will spend $285,000, according to an estimate by Fidelity Investments. LTC expenses would be on top of that.

For advisors, it means looking at the probability of a particular client needing care eventually — genetics and lifestyle can factor in — and evaluating available resources to recommend an option.

Depending on the specifics of your situation, it could make sense to purchase some form of insurance or to self-insure — that is, rely on your own assets — to fund the unpredictable costs related to LTC.

“If people have about at least about $3 million to $5 million in liquid assets and are in their 60s, they can probably use the income from their assets when they need to pay for long-term care,” Wright said.

Other options include leaning on family members or spending down (or shielding) assets to qualify for Medicaid-sponsored nursing-home.

“It very much comes down to your personal situation, family history of needing long-term care and preferences for how and where you might receive care if you need it,” said CFP Katherine Fibiger, a partner and wealth advisor at Stratos Wealth Advisors in Westport, Connecticut.

Even then, it’s tricky to pinpoint a dollar amount involved. And, average costs can vary widely from state to state.

Niv Persaud, CFP and founder of Transition Planning & Guidance in Atlanta, recently estimated an LTC price tag of $300,000 for a female client whose husband has already passed away. The amount includes three years of in-home care, two years in assisted living and three years in a nursing home.

“The number of years in each level of long-term-care service is a guesstimate, since we really don’t know,” Persaud said.

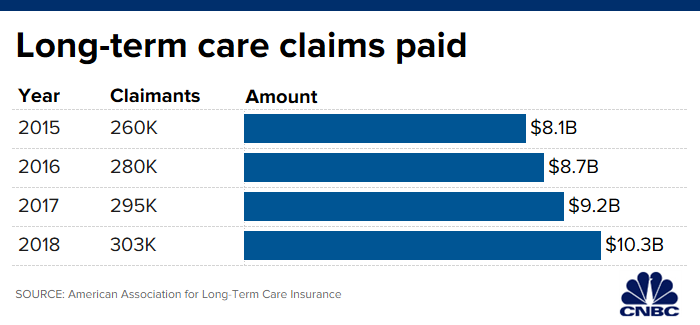

The most straightforward solution — LTC insurance — has become too expensive a proposition for many consumers, contributing to a 60% drop in sales since 2012, according to the LIMRA LOMA Secure Retirement Institute. With claims exceeding expectations, many insurers also have fled the space.

“The offerings have narrowed over the last 10 years while the cost of coverage has risen significantly,” said Chris Griesedieck, managing director at Zemenick & Walker in St. Louis.

“For many policies, the costs rise significantly as the insured ages, and as this occurs, the cost of coverage in relation to their income often makes it unaffordable,” said Griesedieck, whose firm ranked No. 30 on the CNBC FA 100 list.

The average annual LTC premium cost for a 60-year-old couple is $3,400, according to recent data from the American Association for Long-Term Care Insurance. The value of benefits when they reach age 85 would be $343,000 each.

More from Financial Advisor 100:

CNBC ranks to 100 financial advisory firms for 2019

Advisors must change to succeed in next decade

Here are the changes, challenges advisors see ahead

For clients with existing policies whose premiums are becoming unmanageable, it’s worth trying to negotiate with the insurer, Brennan said. For example, in exchange for keeping a lower premium, you could try to lower the policy’s built-in inflation adjustment, or reduce the maximum per-day benefit or duration of those benefits.

Some advisors recommend that clients consider a hybrid policy that combines life insurance with LTC coverage. That can be done through a new purchase or by converting an existing policy — term or whole — to the option.

“If you’re going to have life insurance anyway, you can see if you can protect against long-term-care, too,” said Fibiger, of Stratos.

While the particulars of each policy vary, the idea is that you can tap the death benefit during your lifetime if you need it to pay for LTC. Doing so reduces the amount that your heirs would inherit. Some hybrid options provide LTC coverage beyond the death benefit.

If you’re going to have life insurance anyway, you can see if you can protect against long-term-care, too.

Katherine Fibiger

Partner and wealth advisor at Stratos Wealth Advisors

However, you generally need to be insurable — that is, pass medical underwriting — just as with a straight LTC policy.

You also typically need a pot of money to fund it. Some insurers ask for an upfront lump sum, while others allow you to spread the premium payments over a set number of years.

Also be aware that “chronic illness” riders are different from those for LTC.

“It’s contingent upon your condition being permanent,” Fibiger said. “Long-term care riders are less restrictive.”

Not all advisors are sold on these hybrid policies.

“We’re highly skeptical of the sustainability of the hybrid model,” said Brennan, of Acorn Financial. “There’s not a ton of data out there about whether those paying strategies work over time across a large data sample.

“I think it’s not something we’d ever advise someone to rely on solely,” he added.

Weekly advice on managing your money

Get this delivered to your inbox, and more info about about our products and services.

By signing up for newsletters, you are agreeing to our Terms of Use and Privacy Policy.

Nevertheless, they hold more appeal for consumers than straight LTC policies: In 2018, sales of life-LTC hybrids increased 5% over 2017, according to the LIMRA LOMA Secure Retirement Institute.

Sales for annuities with LTC riders, likewise, have grown, as well, rising to $575 million in 2018, 7% more than in 2017 and more than double the sales from five years earlier, the latest available data show.

For this option, a lump sum is used to purchase the annuity, which promises to pay out a certain amount at a certain point in the future. However, annuities can often come with higher ongoing fees than other investments, and it’s another instance where you need a lump sum of money to make the purchase.

Sometimes a qualified longevity annuity contract, or QLAC, is an option, said Persaud, of Transition Planning. You purchase it using funds from a retirement account such as an individual retirement account or 401(k) plan, and then at a future date that you specify, you get guaranteed monthly payouts from it for the rest of your life (or your spouse’s).

Once you bring long-term care into the equation, anything and everything is on the table.

Matthew Brennan

Partner at Acorn Financial Services

It also lets you exclude the amount from required minimum distributions — which kick in at age 70½ for those retirement accounts — until age 85. When the income stream starts, it can be used however it’s needed (including for LTC costs).

The maximum that can go into a single QLAC is either $130,000 or 25% of the value of your retirement accounts, whichever is less. And, you must start taking the payments by age 85.

Real estate also is an option for funding LTC expenses.

“Once you bring long-term care into the equation, anything and everything is on the table,” said Brennan, of Acorn Financial.

“So you have to consider equity in a home,” he said. “That could mean getting a reverse mortgage, or an equity line of credit that you don’t draw on unless you need care, or the full sale of the home.”

Persaud, of Transition Planning & Guidance, has recommended to one client that she should plan on selling her vacation home at a future date to fund potential LTC costs.

The other aspect that goes into the decision-making often is client experience, advisors say. That is, people who have been caregivers for an elderly parent might be more likely to stretch their budgets to accommodate an LTC insurance option than a wealthy person who has never faced the challenges that come with providing care.

Some people end up trying to move assets out of their ownership so they can qualify for Medicaid, which — unlike Medicare — covers LTC. It’s generally available to people who have no more than a few thousand dollars in assets and meet strict income tests.

However, there’s a “five-year lookback” when you apply for Medicaid. That means any asset transfers made in the five years leading up to the application are considered and could make the applicant ineligible for Medicaid services for a period of time.

As for when people should get serious about exploring the best way to fund those potential later-in-life costs, the half-century mark is a good one.

“I usually recommend people starting looking at it in their 50s,” Fibiger said. “It absolutely should be part of someone’s retirement planning. Whether you should purchase insurance is another conversation, but you at least should have a plan.”